芯片巨頭英偉達(NVDA.US)在「1拆10」拆股後,股價飙升。

華爾街似乎將拆股的AI概念股視為一大利好。在AI浪潮的推波助瀾下,不少AI半導體股都經歷了可觀的升浪,為此拆股後,其每手交易單位的價格變得更加親民,讓更多散戶投資者也能參與其中,繼續為其股價的漲勢添柴加火。

英偉達之後,半導體股博通(AVGO.US)也將在7月中旬「1拆10」。

博通為超大型客戶提供的以太網絡轉換和AI加速器是其人工智能收入的主要推動力,該公司預計於2024財年,此項收入可達到110億美元,而其不久前公佈的截至2024年5月5日止第2財季業績亦超出預期,季度收入為創紀錄新高的124.9億美元,其中AI產品的相關收入達到31億美元,佔其總收入的24.82%,接近博通之前設定的2024財年AI產品收入目標——佔其總收入的25%,而在2023財年,生成式AI僅佔博通半導體業務總收入的15%。

在此帶動下,博通的股價近日大漲,今年以來累計上漲62.17%,在6月12日公佈季度業績之後至今不到五個交易日,博通的股價累計上漲20.53%。

「拆股」神話在兌現。

不過對比於博通以「拆股」來觸達更廣泛投資者,每股179.69美元的晶圓廠商台積電(TSM.US)正在悶聲猛漲。今年以來,台積電累計上漲74.03%,市值達到9,319億美元,已逼近萬億!比博通的市值8,391億美元高出近千億,並已超越全球市值最高的制藥公司禮來(LLY.US),後者得益於減肥藥概念,今年股價累計上漲53.46%,市值達到8,472億美元。

台積電的優勢在哪里?

如果說英偉達的優勢是把握了生成式AI的投資機會,成為各大科技巨頭和科創公司進行AI佈局的奠基者,那麽台積電的優勢比英偉達還要強大,因為它不僅是英偉達最先進AI芯片的代工廠,也是英偉達的競爭對手美國超微公司(AMD.US)和英特爾(INTC.US)的主要供應商。

在客戶們向三大芯片公司紛紛下單的時候,這些訂單一般會落到台積電身上,因為台積電擁有最先進的制程量產能力。縱使英特爾野心勃勃地要發展代工產業,其產能仍與台積電存在差距。

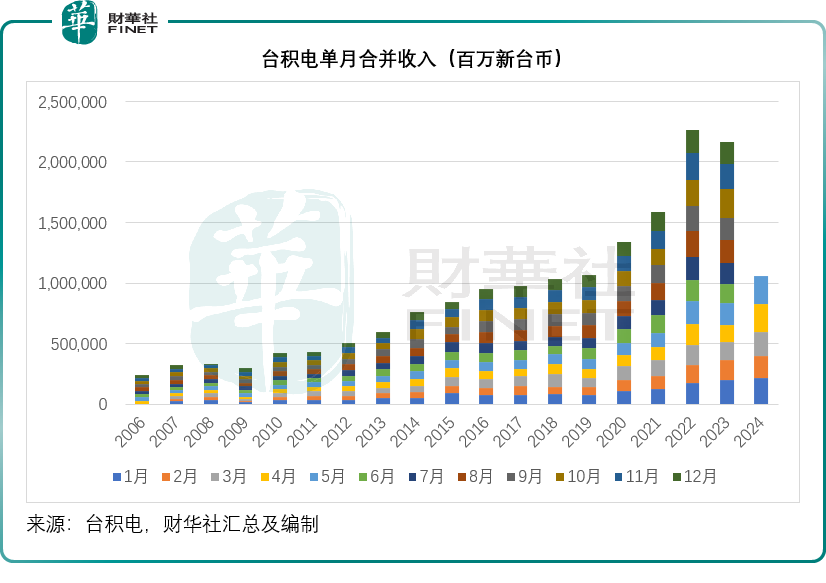

H100需要借助台積電的5納米產能,而英偉達的AI芯片升級版H200/B100,則採用台積電的4納米和3納米制程,台積電的產能一下子爆滿。見下圖,台積電的營收在這兩年大幅度攀升。

儘管英特爾回歸的CEO基辛格正野心勃勃地要在四年内追五個節點,趕超台積電,但就目前的技術和產能而言,台積電仍具有壓倒性優勢。英特爾挑戰英偉達而發佈的AI芯片Gaudi 3,採用的是5納米技術,顯然還需要借助台積電的代工。此外據悉,台積電最近已獲得英特爾即將推出的筆記本電腦處理器系列3納米芯片訂單,繼續通吃三大芯片公司。

台積電董事長及總裁魏哲家在2024年第1季業績發佈會上提到,作為AI應用的重要賦能者,台積電將可從AI強勁需求中得益。他指出,現在幾乎所有的AI創新者都在與台積電進行合作,預計今年來自AI加速器的收入貢獻將增長超過一倍,佔其全年總收入的10%左右。他預計,在未來五年,這些收入將按50%的年復合增長率上升,到2028年佔其總收入的比重將達到20%以上。

因此台積電將是AI發展大潮中的最大得益者,而且它並不局限於英偉達是否成功,AMD、英特爾與英偉達的競爭越激烈,台積電的地位也不會受到影響,因為就技術產能而言,所需的生產技術越先進,台積電越能彰顯其技術優勢。

由此可見,台積電要突破萬億市值也是分分鍾的事。而再追溯產業鏈上遊,另一家供應商也將得益於AI芯片的發展——光刻機供應商阿斯麥(ASML.US)。

阿斯麥會成為下一家拆股的公司嗎?

半導體的生產離不開光刻機,阿斯麥就像光刻機行業的台積電,擁有最先進的技術和最廣泛的客戶群體。

今年以來,阿斯麥的股價累計上漲40.72%,並突破千元關口;按現價1061.38美元計算,其市值達到4,188億美元,已超越LVMH(當前市值3,566億歐元,約合3,822億美元),成為歐洲市值第二高上市公司,與歐洲市值第一的諾和諾德(NVO.US)相差兩千億美元,減肥藥之王諾和諾德今年股價累計上漲37.09%,當前市值為6,271億美元。

總結

2024年,承接2023年,AI和減肥是資本市場追捧的兩大熱門賽道。正如前文所述,兩大減肥藥供應商禮來和諾和諾德,股價累計漲幅均在三成以上;而AI產業鏈的上遊龍頭,股價漲幅更在此之上,阿斯麥累計上漲40.72%,台積電累計上漲74.03%,不過對比於它們的下遊英偉達173.81%的漲幅仍有一定距離。它們是否會追落後?值得留意。

更多精彩內容,請登陸

財華香港網 (https://www.finethk.com/)

現代電視 (http://www.fintv.com)