7月9日,號稱「港股燕窩第一股」的燕之屋(01497.HK)暴漲14.07%,收報12.0港元/股,市值達55.86億港元,股價及市值均創2023年12月12日上市以來的新高。

截至7月9日收盤,燕之屋年初至今股價累計漲幅達36.9%。

值得注意的是,除了燕之屋表現搶眼,長久股份(06959.HK)、美中嘉和(02453.HK)、友寶在線(02429.HK)以及宜明昂科(01541.HK)這5家港股次新股,今日漲幅也都超過了10%。

港股次新股的股價異動或受到其流通股較少及股本過度集中等因素的影響,這種背景下,只有少量的成交量也可能導致股價產生顯著波動。

6月19日,香港證監會發佈公告稱,最近曾就長久股份的股權分佈進行查訊。查詢結果顯示,長久股份存在股權高度集中的情況。

香港證監會還提示,鑒於股權高度集中於數目不多的股東,即使少量股份成交,該公司的股份價格亦可能大幅波動,股東及有意投資者於買賣該公司股份時務請審慎行事。

從基本面角度來看,燕之屋深耕的燕窩賽道增長前景是可期的。

據公開資料顯示,燕之屋始於1997年,是中國燕窩賽道的「領頭羊」。

根據北京中研世紀咨詢有限公司近期統計顯示,燕之屋已連續八年位居高端燕窩全國銷售第一。此外,2024年天貓年中開門紅期間,燕之屋再次奪得滋補類店鋪累計GMV排名第一名。

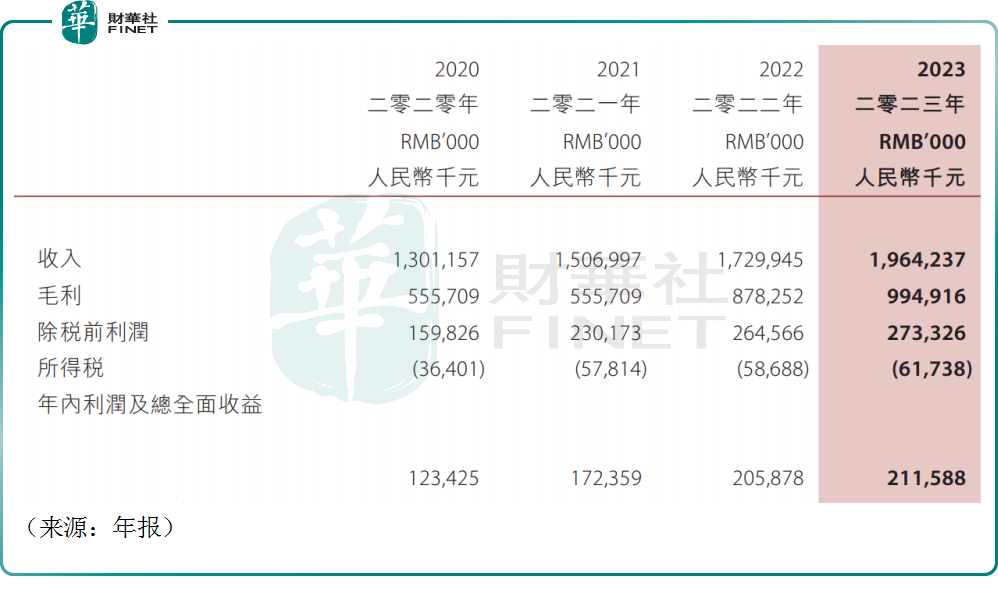

伴隨著「她經濟」的崛起,燕窩消費持續攀升,燕之屋業績表現不俗。2023年,燕之屋毛利率高達50.7%,公司針對的是高淨值女性客戶,令不少消費品企業豔羨。

2023年,燕之屋實現營收19.64億元(人民幣,下同),同比增長13.5%,實現淨利潤2.12億元,同比增長2.8%。公司近些年營收利潤基本處於上升通道,但淨利潤增速明顯不及應收。

淨利潤增速放緩,或受成本端產生的影響。2023年,燕之屋的銷售及經銷開支5.63億元,這其中相當一部分是廣告開支,而2023年公司研發開支僅為0.26億元,燕之屋過度依賴廣告營銷,也遭到一些投資者的诟病。

據悉,自2008年起,燕之屋就邀請劉嘉玲、林志玲、趙麗穎、金晨等知名明星陸續代言,公司試圖建立「燕之屋等於燕窩」的品牌認知,佔領客戶心智。

2024年,公司更是先後官宣鞏俐、王一博為全球品牌代言人,實現對不同年輕圈層女性用戶的精準營銷,相關話題屢屢衝上微博熱搜。

通過營銷「轟炸」以換取收入增長的策略,在過往幫助燕之屋從一眾競爭對手中脫穎而出,成為銷冠。但同時也帶來營銷成本的高企,公司的利潤空間被大量吞噬,相關業務模式是否具備長期的可持續性,外界的質疑聲音並不少。

此外,公司面臨的競爭十分激烈。近年來,小仙炖、燕之初、燕小廚等一眾品牌紛紛入局並快速成長,瓜分燕窩賽道的市場份額,料將對燕之屋的業務造成一定壓力。

燕窩賽道亦較為分散,方正證券研報顯示,中國的燕窩行業CR5僅為11.9%,其中燕之屋市佔率5.8%。當前燕窩行業市場規模400多億,市場參與者多而不專,行業集中度低。

不過,該機構認為,燕之屋在燕窩行業的品牌力積累已久,產品運作經驗豐富,渠道覆蓋兼具廣度和深度,公司有望通過產品的不斷創新以及品牌力的持續提升佔領消費者心智,實現市佔率的提升。這或許也是公司未來最大的看點。

海通證券也在7月5日發佈燕之屋首次覆蓋報告,結合公司去年業績和近期股價表現,認為公司對應合理價值區間13.86至15.52 港元,首次覆蓋給予「優於大市」評級。

從宮廷禦膳到走進尋常消費者餐桌,一直以來,燕窩都是追求滋補養生人士的高端首選,長期來看,在顔值經濟盛行的趨勢下,燕窩行業的景氣度無虞,其潛在消費群體不可小觑。

更多精彩內容,請登陸

財華香港網 (https://www.finethk.com/)

現代電視 (http://www.fintv.com)