在2024年7月22日晚,全球芭比迷們的寵兒——美泰公司(MAT.US),其股價如火箭般衝天而起!一度飙升超過20%,最終收市價為18.68美元,與前一交易日相比,漲幅高達15.10%。隨著股價飙升,美泰的總市值重返60億美元重要關口,並進一步升至64億美元,折合人民幣約466億元。

推動股價造好的原因,與一則傳聞有關:傳聞頂級奢侈品集團LVMH(LVMUY.US)旗下的私募基金L Catterton想收購美泰。

在瞬息萬變的資本市場,美泰股價的飙升並非無風起浪。這背後與一則熱門傳聞有關:國際頂尖奢侈品巨頭LVMH(LVMUY.US)旗下的私募基金L Catterton,正醞釀著一場對美泰的收購計劃。

財華社發現,這已經不是第一次傳言LV想收購美泰,2022年4月時就盛傳美國私募公司Apollo Global和L Catterton正與美泰,想以78億美元的價格收購這家納斯達克上市公司。

見下圖,2022年4月受有關消息帶動,美泰的股價曾突破25美元水平,其後傳言又不了了之,美泰的股價下滑。

美泰的潛在買家還有誰?

據悉,不僅LV對美泰表現出濃厚的興趣,市場上亦有多家同行業競爭者積極與美泰接觸,意圖通過合並構建更為龐大的玩具產業帝國。

在這次LV私募基金被傳與美泰接洽談論私有化的同時,有說市值比美泰高出三成的玩具巨頭孩之寶(HAS.US)一直與美泰商討合並。

關於孩之寶與美泰的合並傳聞,儘管多年來持續被提及,但始終未能實現。然而,面對LV的積極進逼,孩之寶或許感受到了緊迫的壓力。據路透社引述相關知情人士的消息,孩之寶或正考慮提交收購要約。

去年,美泰與孩之寶達成了合作協議,就兩者最受歡迎的品牌,包括美泰的芭比品牌大富翁遊戲和孩之寶變形金剛品牌紙牌桌遊,創建合作品牌。

除了孩之寶外,生產「反芭比」Bratz娃娃的MGA於2019年6月也曾有意合並美泰。有報道指出,MGA的CEO曾致信美泰,指出美泰的若幹財務問題,包括經營虧損、債務負擔增加以及股東權益下降,並表達了合並後自己擔任美泰董事會主席和CEO的意向。

不過,有關收購要約被美泰高管以有關收購「不符合美泰及其股東最佳利益」為由拒絕。

美泰估值為啥這麽便宜?

今年以來的表現,孩之寶股價一路上漲20.17%,讓人眼前一亮。然而,美泰的股價卻沒這麽給力,即使算上7月22日因收購傳聞引發的15%漲幅,年内依舊下跌了1.06%。看看下面這張表格,你會發現華爾街對美泰的市盈率估值預期,遠不及孩之寶那麽高。

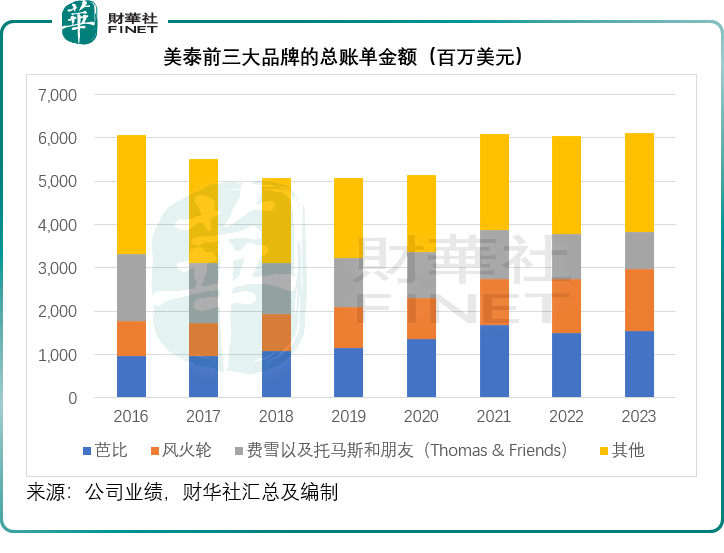

美泰是一家專注於通過IP價值附加實現變現的零售企業。其持有的產品組合廣泛而多元,涵蓋了多個知名品牌和系列。其中,玩具娃娃類别擁有芭比、美國女孩、迪士尼公主、冰雪奇緣系列娃娃等知名品牌;嬰幼兒及學前兒童玩具類别則包括費雪、託馬斯和朋友等備受歡迎的品牌;在玩具車領域,美泰擁有風火輪、賽車總動員等知名品牌;此外,美泰還涵蓋了卡通角色、建築玩具套裝、遊戲以及其他類别,如宇宙大師、侏羅紀世界等品牌。

在美泰的營收構成中,芭比和風火輪兩大品牌佔據了顯著地位。根據數據顯示,2023年芭比和風火輪分别貢獻了美泰總營收的25.20%和23.48%,成為公司最主要的收入來源。具體情況可參見下圖所示。

值得注意的是,去年暑假,電影《芭比》所引發的廣泛關注和熱烈討論,對於美泰的芭比產品銷售產生了顯著的正面宣傳效應。

財華社發現,2023年下半年,芭比的總賬單金額按年大幅增長20.90%,至10.78億美元,增幅遠高於上半年的-23.25%。

受「芭比」旋風帶動,美泰的2023年下半年收入按年增長12.09%,經調整毛利率按年提升了3.98個百分點,至49.96%;經營利潤率亦按年上升3.35個百分點,至18.45%。

不過,這一「魔法」似乎無法持續到2024年。

美泰2024年第1季的業績顯示,芭比的賬單收入僅持平為1.78億美元,美泰的季度淨銷售收入整體下降1%,至8.1億美元。

值得留意的是,美泰於2017年-2019年期間持續錄得虧損,而該公司也採取成本優化政策來改善盈利能力。

2024年第1季的成本削減措施似乎奏效,儘管季度收入減少,但其經調整率卻得到830個基點的提升,主要得益於庫存管理成本下降、成本優化計劃、產品組合優化以及降低供應鏈成本的措施。受此影響,其季度經調整經營虧損進一步縮小73%。

儘管全球品牌營銷競爭日趨激烈,美泰持續改善成本的努力或才是買家所贊賞。

財華社猜測,LV旗下私募的收購或著意於財務投資的可能性較大,美泰估值偏低和業績狀況正在改善或是其重要考慮,不過玩具同行孩之寶和MGA或更在意品牌的結合所帶來的協同效應。

美泰將在7月23日美國時間公佈2024年第2季度業績,對其未來的業績展望以及收購可能會有更多啓示,其股價也可能跟隨這些消息大幅波動。

更多精彩內容,請登陸

財華香港網 (https://www.finethk.com/)

現代電視 (http://www.fintv.com)