美國最新公佈的通脹數據大致符合預期。

最新的數據顯示,美國2024年7月份年度通脹率連續第四個月放緩,至2.9%,這是2021年3月以來的最低,低於上個月的3%,也低於預期的3%,其中佔比較大的居住物價通脹率由上個月的5.2%下降至5.1%應是主要原因。

與上個月相比,消費物價指數增加0.2%,較上個月的-0.1%回升,但符合預期,其中居住成本上升0.4%是主要的上漲因子。

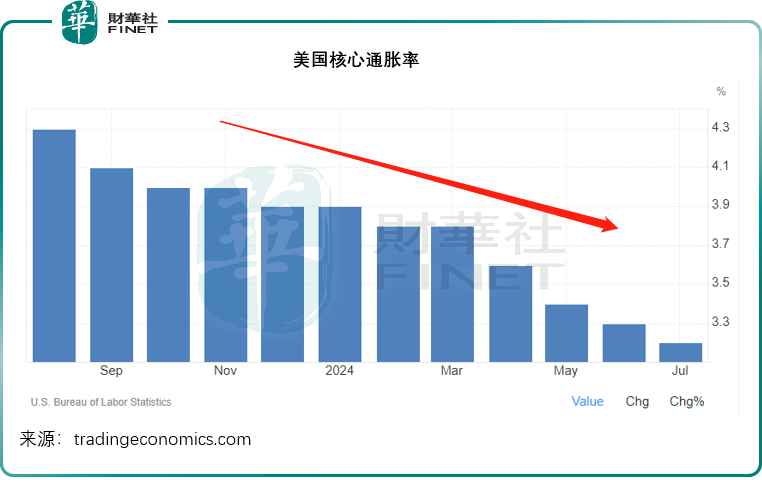

扣除波動較大的食品和能源後的核心通脹率,於2024年7月進一步下降至3.2%,是三年最低,符合市場預期,見下圖。

另一方面,稍早時公佈的7月份生產價格指數微升0.1%,低於市場預期的升幅0.2%。

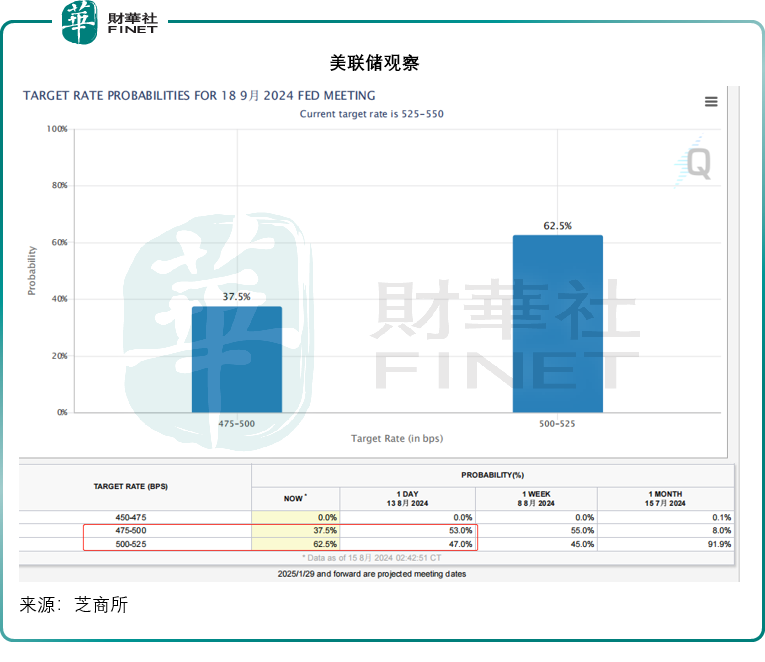

近期數據令市場對於美聯儲九月份或大手降息50個基點的預期降溫。見下圖,在公佈通脹數據之後,預期美聯儲降息25個基點的比率由一日前的47.0%上升至62.5%,預期降息50個基點的比率由一日前的53.0%下降至37.5%。

市場現在普遍預期美聯儲九月議息會議將降息,只是對降息幅度存在分歧,在公佈通脹數據之前,預期降息25個基點與預期降息50個基點的投資者比例相當。而剛剛公佈的通脹數據大致符合預期,似乎缺乏顯著收縮以便讓美聯儲迫切加息以刺激經濟的驚喜,因此投資者開始傾向於降息25個基點這一預期。

美元指數維持平穩,但美國10年期國庫券息率則上升,債市下降(息率與價格呈反向走勢),資金或流向股市。

華爾街三大指數道瓊斯工業平均指數(DJI.US)、納斯達克指數(IXIC.US)和標普500指數(SPX.US)當日分别上漲0.61%、0.03%和0.38%,主要受大型科技股走勢影響,而在缺乏宏觀消息的推動下,大型科技股近日走勢主要與其自身的消息面有關,例如谷歌(GOOG.US)受分拆憂慮拖累,股價下跌2.35%;而前端時間較弱的英偉達(NVDA.US)和蘋果(AAPL.US)則逐步修復其之前的失地。

前景如何?

2024年8月15日(周四)將公佈美國零售銷售數據,或將反映當前的消費情緒是否受到前期加息的影響,以及在高利率下消費增長的韌性,也將對9月的議息會議帶來啓示。

基本可以肯定的一點是,美國的通脹已受到控制,同時經濟增長也有放緩迹象,美聯儲要保障遏制通脹的成果,或不得不降息以支持經濟增長。

當前的華爾街股市仍主要為AI概念主導——在AI火熱的時候,這些資金衝入AI概念股;當大家對AI投資過熱感到擔憂時,資金又奮力地從這些AI概念股衝出,導致AI概念股的大幅波動,而由於這些股份都是指數的重磅股,也影響到大盤的走勢。

這兩年,由於美聯儲加息令資金成本維持在高水平,對衝基金和風投基金在投資創新項目時變得謹慎。與此同時,火熱的AI投資大幅推高了AI初創企業的估值,也讓對資金成本越來越斤斤計較的風投基金在跟投AI初創企業的後期融資時越來越猶豫。

另一方面,巨型科技股持有巨額現金正無處可投,而近幾個月的大裁員讓它們的運營預算變得松動。與其向不確定前景的項目投入巨額,何不直接從這些初創公司挖角來得經濟實惠,畢竟一個相對成熟的AI項目,融資輪或也數以十億計,還不知道能否安全退出,而挖入核心人物和這名核心人物可以帶來的授權,或只需一兩億,而且項目不成還能轉到其他開發部門,物儘其用。

例如微軟(MSFT.US)今年上半年集體挖角AI初創公司Inflection AI的高管,亞馬遜(AMZN.US)也不遑多讓,搶奪AI獨角獸Adept的核心技術團隊,留給之前對這些項目投入巨資的風投的,只剩下空殼。

原本財務實力就不夠這些賺錢機器科技巨企競爭,還要面對高利率所帶來的估值危機,手頭上不少項目難覓對手方而無法出售,這些風投機構這兩年也是過著苦日子。

若美聯儲進入降息周期,全球資金流或變得松動,或多少能緩解這些困境。

更多精彩內容,請登陸

財華香港網 (https://www.finethk.com/)

現代電視 (http://www.fintv.com)